Property UpdateReal Estate Investing Advice & Strategies From Experts You Can Trust2025-08-28T22:56:39Zhttps://propertyupdate.com.au/feed/atom/WordPressBrett Warren<![CDATA[Spring Awakening: Why 2025 Could Be a Defining Season for Australia’s Property Market]]>https://propertyupdate.com.au/?p=1911112025-08-28T22:55:51Z2025-08-28T09:30:10ZEvery year, spring breathes new life into Australia’s property markets. It’s the season that shapes how the year closes and often sets the tone for the year ahead.

New analysis from Domain indicates that recent cash rate cuts, boosted buyer confidence, and spending power are setting the stage for a supercharged spring selling season.

The data, which looks at the last decade of market trends, reveals:

Spring price surge: Houses sell for a 2.6% premium in spring compared to winter.

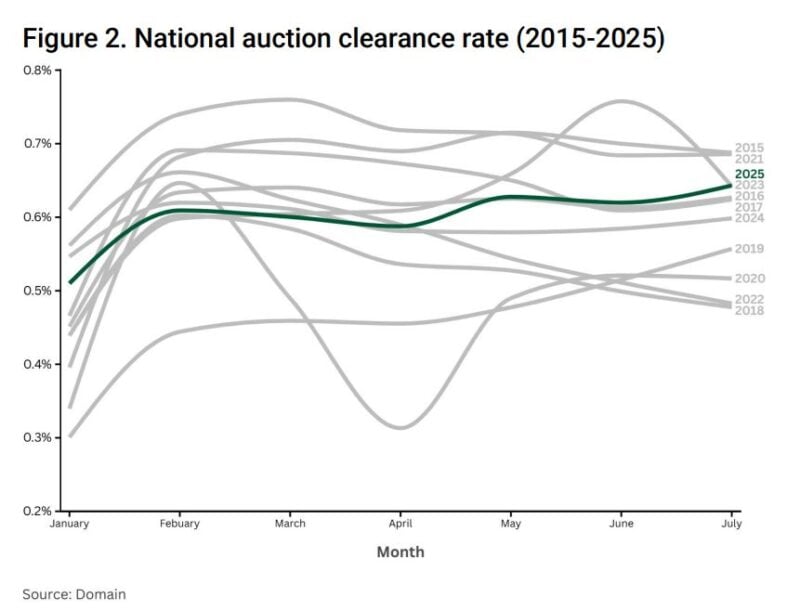

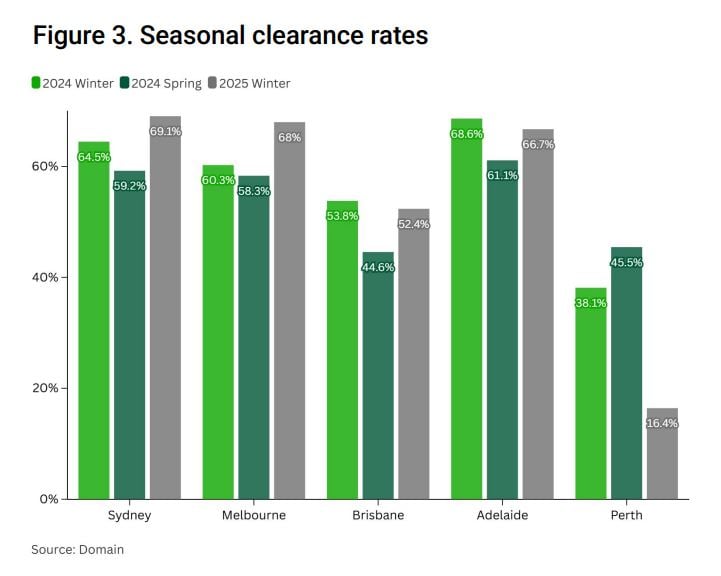

Strong winter momentum: July clearance rates for 2025 have reached their strongest point in a decade, primarily driven by Sydney and Melbourne (69.1% and 68% respectively, Table 2). Sydney and Melbourne’s clearance rates for winter 2025 have already surpassed spring 2024, demonstrating the renewed momentum in the market.

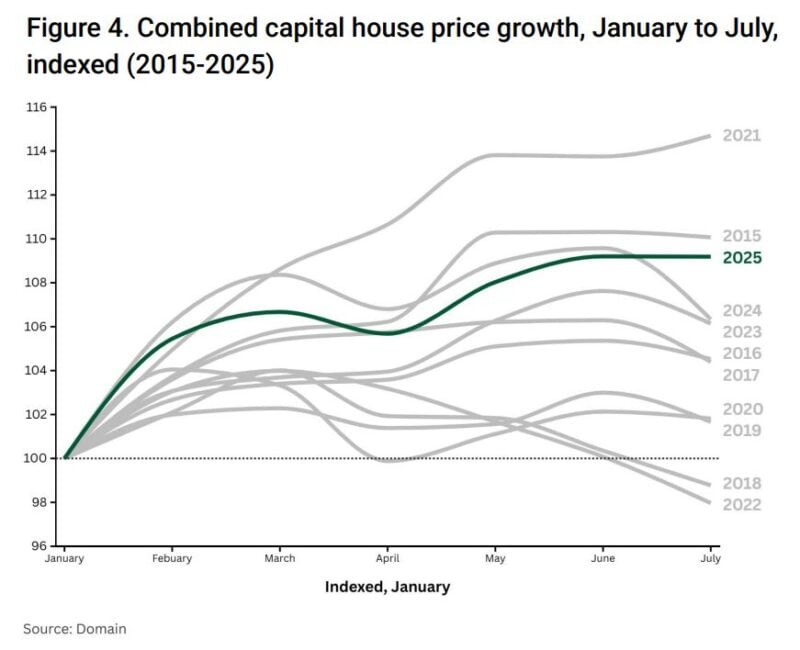

Sustained growth in 2025: The combined capital median house price rose 9.2% between January and July 2025 (Table 3), marking the third-highest January-July growth in the last decade.

As Dr Nicola Powell, Chief of Research and Economics at Domain, puts it:

“Spring is the season that sets the tone for the year’s close. It delivers more choice for buyers, greater activity for sellers, and firmer price growth. But with more listings comes more competition, so strategy and presentation matter more than ever.”

The numbers don’t lie: Spring’s seasonal power

Looking at 10 years of data Domain's research reveals that four patterns stand out:

1. Listings always surge.

On average, the number of homes for sale jumps 5.9% between winter and spring.

By summer, stock typically falls back 7.1%. It’s the sharpest seasonal lift of the year.

10 year average difference in Spring vs Winter performance (2015-2025)

Nationally, transactions rise 8.4% in spring compared to winter, making it the busiest season despite autumn sometimes offering more total listings.

Cities like Canberra (+12.8%), Hobart (+12.2%), and Perth (+10.7%) lead this charge.

3. Auctions dominate.

Auction volumes rise by a staggering 31% compared to winter, and nearly 65% above summer.

While autumn has the highest clearance rates (61.5%), spring’s sheer volume cements it as the auction season.

4. Prices strengthen.

The average price bump between winter and spring is 2.6%, compared to just 0.4% from autumn to winter, and 0.2% from spring to summer. Brisbane, Canberra, and Hobart consistently record the largest spring price gains (around 3%).

In short, spring reliably means more stock, more activity, and higher prices.

A tale of two markets: supply splits the capitals

However, Spring 2025 isn’t starting on level ground. Supply trends have diverged across the country, reshaping local dynamics:

Sydney: Listings remain strong, up 14.6% year-on-year, keeping buyer choice high. This sustained supply may temper runaway price growth but also signals healthy, competitive conditions.

Melbourne: Listings are down 10.2% after peaking at record highs in late 2024. Reduced choice is swinging conditions back towards sellers and firming prices.

Adelaide & Perth: After strong supply earlier in the year, stock has tightened again. This will likely reignite competition and put pressure back on prices.

Brisbane: Inventory is marginally lower (-1.7%) but remains well below its five-year average, keeping the market tight.

Hobart & Darwin: Both cities have seen sharp falls in listings (-16.2% and -36.3% respectively), suggesting limited choice and likely upward price pressure.

Dr Powell notes:

“Supply is the hidden lever in market performance. Where listings fall, competition heats up quickly, and where they rise, buyers regain some power. This spring will expose just how uneven conditions are across our capitals.”

Clearance rates: demand proves its strength

If auctions are the pulse of demand, then 2025 is beating strongly. Domain's auction results show...

July recorded the third-highest national clearance rate for that month in a decade.

Sydney (69.1%) and Melbourne (68%) have delivered some of their strongest winter results in 10 years, setting the stage for a buoyant spring auction season.

Adelaide and Brisbane are also trending near the top of their historical ranges, while Perth has been the outlier, with a very low winter clearance rate of 16.4%.

That resilience tells us something important: despite higher stock levels earlier in the year, underlying buyer demand remains robust, fuelled by cheaper borrowing costs.

Prices: momentum already building

While spring usually delivers the strongest seasonal bump, this year prices are already running hot according to Dr. Powell.

Between January and July 2025:

Combined capital city median house prices rose 9.2%, the third-highest January–July growth in the past decade.

This growth comes despite higher inventory early in the year, a sign that demand is deep enough to absorb stock and still push prices higher.

Dr Powell adds:

“We’re already seeing momentum build in house prices thanks to multiple rate cuts. The big question is whether spring’s seasonal surge will add fuel to the fire.”

Why Spring 2025 could be a turning point

Put it all together and you have a fascinating setup:

Rate cuts have revived borrowing power and buyer confidence.

Supply dynamics are uneven, tilting markets differently across capitals.

Clearance rates show buyers are active and ready to compete.

Price momentum is already running strong.

If the usual spring surge in listings collides with reinvigorated demand, we could see one of the strongest spring markets in years.

For investors, this means bracing for heightened competition, but also recognising that well-chosen assets in undersupplied cities may accelerate in value.

Key takeaways for buyers, sellers, and investors

For buyers: Expect more choice, but also more competition. Be finance-ready and decisive when the right property comes up.

For sellers: Presentation and pricing strategy are critical. Spring delivers the most eyeballs, but you’ll also face the fiercest competition from other vendors.

For investors: Watch city-specific supply trends. Melbourne and Hobart are tightening, while Sydney still offers deep stock — but both dynamics can work in your favour depending on strategy.

The bottom line

Spring always matters in Australian real estate.

But this year, with rate cuts amplifying demand, supply diverging across capitals, and momentum already building, it could matter more than ever.

As Dr Nicola Powell sums it up:

“Spring 2025 is more than just another seasonal lift, it’s a critical test of whether the housing market’s strongest seasonal patterns will combine with policy tailwinds to reshape momentum heading into the new year.”

In my view, this spring is not just about renewal; it’s about reset.

And those who understand the nuances of supply, timing, and competition will be the ones who benefit most.

]]>0Dorian Traill<![CDATA[Why the RBA Won’t Cut Rates in September – But Borrowers Still Have Opportunities]]>https://propertyupdate.com.au/?p=1911552025-08-28T22:56:39Z2025-08-28T07:30:32ZAustralia’s inflation story just took an interesting twist.

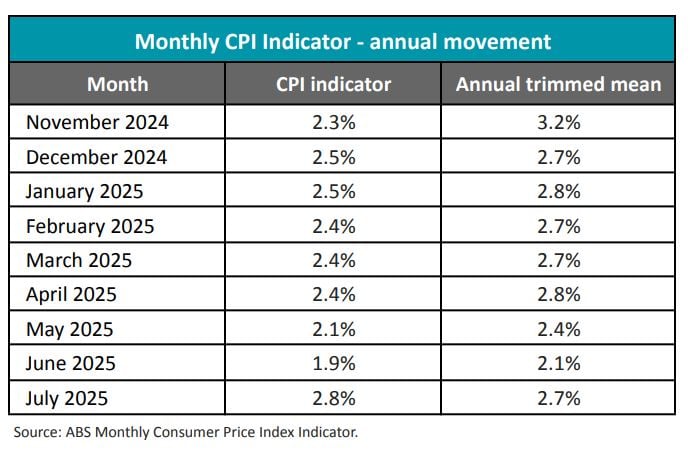

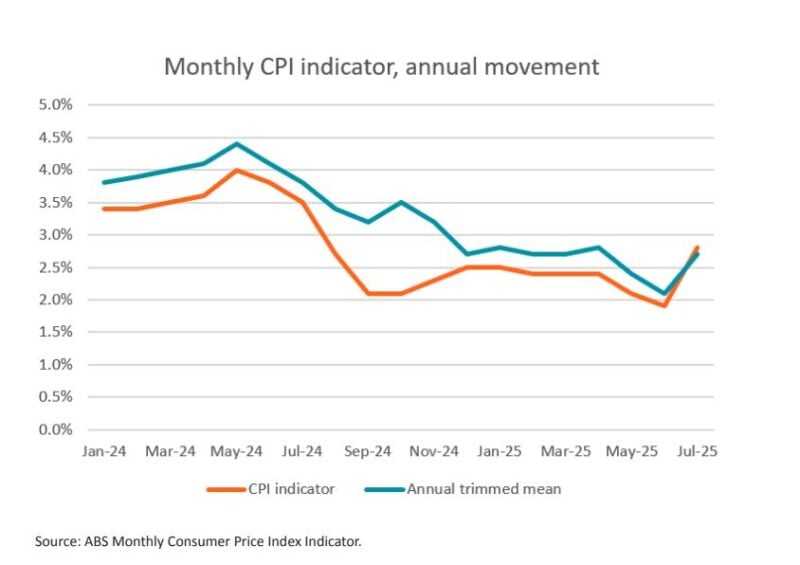

After months of trending down, headline inflation nudged higher in July: lifting to 2.8% from June’s 1.9%.

That may not sound like much, but it’s the first rise we’ve seen in the monthly CPI series since late 2024.

So, what’s driving it?

Electricity prices surged by over 13% in the past year, partly thanks to July’s price hikes and the delay in government rebates for NSW and ACT households.

Add in pricier holiday travel during the school holidays, and suddenly inflation has momentum again.

For property investors and homeowners, the question is: what does this mean for interest rates and, therefore your mortgage?

Why a September rate cut is off the table

The Reserve Bank was never expected to rush into another move at its 30 September meeting, but this uptick in inflation has shut the door completely.

As Sally Tindall, Canstar’s Research Director, puts it:

“The possibility of a September cash rate cut was a long shot at best, however, this round of monthly data squashes pretty much all hope of back-to-back moves."

The RBA Board has already signalled it prefers a gradual easing cycle.

They’ll want to see the September quarter CPI numbers (due 29 October) before taking action.

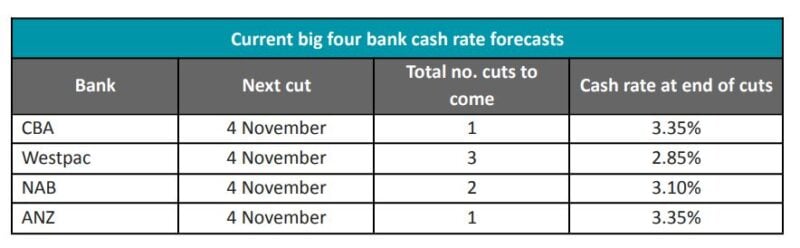

If the trend is still under control, then the November 3–4 meeting is shaping as the next opportunity.

The big banks agree. CBA, NAB, Westpac and ANZ all expect November to be the month, though their forecasts for how far cuts will go vary.

Westpac sees three more cuts, potentially taking the cash rate to 2.85%.

Here’s the real twist: despite inflation ticking higher, mortgage rates are still drifting lower.

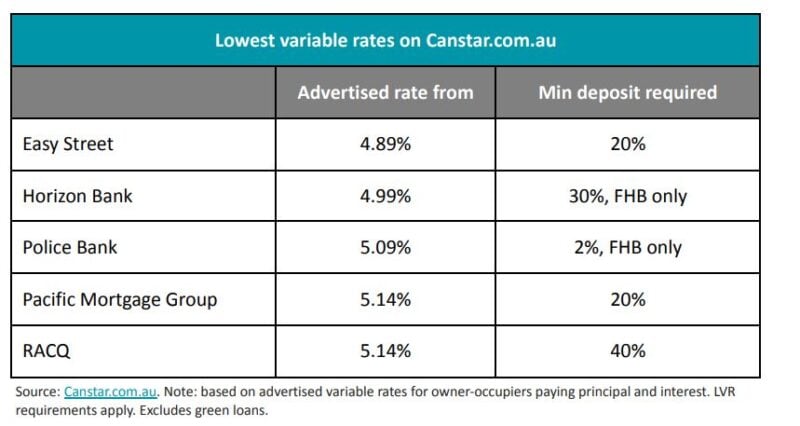

Since the RBA’s August cut, 88 lenders have trimmed their variable rates, with most passing on the full 0.25% reduction.

Easy Street has dropped to 4.89%, the lowest variable rate on the market right now. That’s ultra-competitive, but the offer is time-limited, available only for applications lodged before 10 October and settled by 10 December.

It’s not just Easy Street. Almost 30 lenders are now offering at least one variable rate under 5.25%, which is great news for borrowers willing to shop around.

What this means for property investors

If you’re a property investor waiting for the RBA to hand you another cut, don’t hold your breath, at least not until November. The RBA is being cautious, and rightly so.

I believe this offers a window of opportunity for property investors as we’re seeing what some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

Continued rapid population growth is putting pressure on housing.

An acute undersupply of dwellings,

A chronic shortage of skilled labour, making new development slower and more expensive.

Inflation has moderated, now sitting within the RBA’s target range.

Interest rates will keep falling – bringing more buyers into the market

Government first homebuyer incentives will pour fuel on the flames of our undersupplied housing market after October.

Are you clear on how to take advantage of these market conditions - that’s where our Complimentary Wealth Discovery Session comes in. We’re offering you a 1-on-1 chat with a Metropole Wealth Strategist to help you:

Clarify your financial goals

Understand how macro trends affect your position

Build a personalised, data-driven property strategy

Get ahead of the curve — before everyone else piles in

There’s no cost, no obligation — just practical, tailored guidance based on decades of experience.

Click here now to book your free Wealth Discovery Session

]]>0Adam Hubbard<![CDATA[Why Community Has Always Been at the Heart of Australian Housing and Why That’s More Relevant Than Ever]]>https://propertyupdate.com.au/?p=1906862025-08-28T02:45:12Z2025-08-28T06:30:48ZAustralia has always been a nation that values connection, and this is now evident in our housing.

Sure, most of the media commentary focuses on property values, interest rates, and auction clearance rates.

And while those metrics are obviously important for us as investors, there’s a more fundamental force quietly shaping our cities and influencing long-term capital growth that investors need to understand, and that is: community.

It’s a timeless idea, but one that’s now evolving in a very modern way.

Today, community isn't just something you hope to find in a suburb; it's being deliberately designed into the very fabric of our new neighbourhoods.

So let’s take a closer look at how the idea of community has shaped Australian housing in the past, and why it’s becoming more critical to our property decisions than ever before.

From quarter-acre blocks to connected living

Once upon a time, the great Australian dream was all about the quarter-acre block: a detached home on the city fringe, often separated from real amenities and entirely dependent on the car.

It was a symbol of aspiration and ownership, but in hindsight, many of those neighbourhoods were physically isolated.

There was privacy, yes, but not necessarily connection.

Today, we’re seeing a decisive shift.

Homes are becoming smaller and denser, but the surrounding environment is becoming more important.

People are placing greater value on what’s available outside their front door: parks, walking trails, cafés, schools, and a sense of local vibrancy.

It’s no longer just about having a house. It’s about living in a place, a neighbourhood that supports lifestyle, health, convenience, and social connection.

Masterplanned communities are being reimagined.

The way new suburbs and housing estates are being developed is changing, and in a good way.

Where earlier developments focused heavily on lot sizes and road layouts, today’s masterplanned communities are being shaped by community values.

We’re seeing smarter, more intentional planning that puts green spaces, playgrounds, local centres, and shared spaces at the heart of the neighbourhood.

This isn’t just a design choice, it’s a response to what buyers are actually seeking.

In an age of digital fatigue and post-pandemic disconnection, Australians want to live somewhere they feel part of something bigger than just their four walls.

And that presents a huge opportunity, both for developers who get it right and for investors who understand how this kind of social infrastructure supports property demand.

The rise of the 20-minute neighbourhood

One of the most significant planning trends today is the emergence of the 20-minute neighbourhood, where residents can access most of their daily needs within a short walk or bike ride from home.

It’s a concept that ticks a lot of boxes:

It reduces commute stress

Encourages local spending

Improves walkability

And most importantly, it helps foster genuine community interaction

This model is increasingly being built into the DNA of new developments.

And it aligns well with how people want to live today, especially families, downsizers, and young professionals who want convenience without sacrificing quality of life.

From an investment point of view, these neighbourhoods are incredibly resilient.

They retain value in downturns, they’re more appealing to long-term renters, and they often enjoy a higher rate of capital appreciation over time.

Walkability is the new location metric.

We’ve all heard the saying: location, location, location.

But in today’s market, walkability is just as powerful a value driver.

People want to live in places where they can comfortably walk to the local café, school, park, or even just the corner shop.

But walkability isn’t just about geography, it’s about design.

Shaded pathways, safe pedestrian crossings, ample seating, thoughtful landscaping- these features make walking not only possible, but pleasant.

And when you make it easier for people to spend time outdoors, they’re more likely to engage with their neighbours, support local businesses, and develop a stronger attachment to the area.

In fact, research consistently shows that residents in walkable neighbourhoods are more physically active, socially connected, and report higher levels of life satisfaction.

That matters. Because happy residents are sticky residents, and sticky residents are good news for long-term property values.

Community-led design is gaining momentum.

Another major shift we’re seeing is the move toward community-led development.

Rather than imposing a one-size-fits-all design from the top down, progressive developers are now involving residents from the outset.

This means inviting locals to help shape public spaces, provide feedback on infrastructure, and even co-create community events or initiatives.

It’s a more collaborative model, and it works.

When people feel they have a stake in shaping their environment, they’re more invested in its success.

They’re more likely to participate, take pride in their neighbourhood, and support local improvements.

Some developers are even offering grants to support grassroots projects, running local sporting events, or supporting residents' associations, not just as a PR strategy, but as a way to foster genuine social cohesion from day one.

What does it all mean for property investors?

It means the most successful long-term property plays won’t just be in the suburbs with the best infrastructure, but in communities that offer a complete living experience.

Here’s what I recommend you look for:

Suburbs with clear urban planning and masterplans that prioritise walkability and green space

Developments that include or are near cafés, parks, schools, and local retail

A strong emphasis on public interaction zones, not just housing density

Signs of resident engagement and a well-run community development program

These are the areas that will attract long-term owner-occupiers, create demand from tenants, and perform well over the next property cycle, regardless of short-term market noise.

Final thoughts

The idea of community in Australian housing is nothing new, but its importance has never been more central to both how we live and how we invest.

As our cities evolve, it’s clear that people are searching for more than just affordability or proximity.

They want a sense of place. They want belonging. They want the real Australia, not just a house, but a home within a community.

And the best part? The suburbs and developments that get this right will outperform. Not just in lifestyle but in value.

So next time you're looking at a property, don’t just ask what the house is worth.

Ask what the neighbourhood is worth.

Because that’s where the real long-term value lies.

]]>0Michael Yardneyhttps://michaelyardney.com<![CDATA[[PODCAST] Planning Australia’s Future: It Starts with Where We Live, with Ross Elliott]]>https://propertyupdate.com.au/?p=1910732025-08-27T01:17:57Z2025-08-27T22:00:12ZToday I’m joined by Ross Elliott, a respected urban thinker and commentator, and we discuss something most politicians and planners are ignoring: thedanger of concentrating 70% of Australia’s population into just eight capital cities, and doing it without a real plan.

We explore the challenges of infrastructure, the concept of the missing middle in housing, and the need for a national settlement strategy to address the growing population and its impact on quality of life.

Whether you're a property investor, policymaker, or simply someone sitting in bumper-to-bumper traffic wondering where it all went wrong, this episode of the Michael Yardney Podcast is going to challenge the way you think about growth, planning, and the future of our cities.

Takeaways

Australia's population growth is concentrated in a few major cities.

High-density living does not necessarily reduce traffic congestion.

There is a significant gap in housing supply and demand.

The concept of the 'missing middle' in housing is contentious.

Infrastructure development has not kept pace with population growth.

Regional centers can offer a better quality of life than major cities.

Government policies need to address urban planning holistically.

Decentralization strategies have not been effectively implemented in Australia.

Community opposition often hinders new housing developments.

A national settlement strategy is essential for sustainable growth.

Win a hard copy of Michael Yardney's Guide to Investing. Everyone wins a copy of a fully updated property report –What’s ahead for property for 2026 and beyond.

Also, please subscribe to my other podcast Demographics Decoded with Simon Kuestenmacher – just look for Demographics Decoded wherever you are listening to this podcast and subscribe so each week we can unveil the trends shaping your future.

]]>0Michael Yardneyhttps://michaelyardney.com<![CDATA[Love or Leverage? How Soaring House Prices Are Trapping Couples Together]]>https://propertyupdate.com.au/?p=1910112025-08-28T22:56:27Z2025-08-27T09:30:29ZAustralia’s housing market isn’t just about affordability, wealth creation, or investment returns.

Believe it or not, it’s also quietly reshaping some of the most personal aspects of our lives: love, relationships, marriage, and family stability.

We’ve long discussed how demographics influence housing. But what’s less often recognised is how housing costs, in turn, influence our personal choices.

In fact, new research suggests that soaring house prices may be locking people into relationships, even unhappy ones, not because couples are more in love, but because they can’t afford to split up.

As demographer Simon Kuestenmacher explained in the latest episode of our Demographics Decoded podcast:

“The financial economic argument is rock solid. Divorce comes with obvious costs: lawyers, moving, and most significantly, running two households instead of one. Even if housing was cheap, two households cost more.”

In other words, the property market isn’t just about where we live. It’s influencing whether we stay together.

For weekly insights subscribe to the Demographics Decoded podcast, where we will continue to explore these trends and their implications in greater detail.

While on paper, separating sounds simple: two people decide to go their own way, in practice, the costs quickly mount.

Legal fees: Divorces involve lawyers, mediators, and paperwork, none of which are cheap.

Moving expenses: Finding and furnishing another property comes with significant upfront costs.

Running two households: Rent or mortgage repayments, utilities, internet, furniture, and even small things like buying another toaster or fridge.

These costs are manageable when housing is affordable.

But today, when median house prices are many multiples of income and rents are at record highs, doubling your housing needs can be financially crippling.

As Simon pointed out, “It is always cheaper to run one household than two. Even if the dwellings are smaller, the costs accumulate. It’s a massive disincentive to leave.”

This helps explain why Australia’s divorce rate has been steadily declining, now at its lowest level since no-fault divorce was introduced in 1976.

In big cities, Sydney, Melbourne, and Brisbane, where housing is most expensive, divorce rates are even lower.

Why now is different

Interestingly, this trend contrasts with what happened during previous periods of financial stress.

During the 1990s recession, divorce rates actually rose as household stress spilled into relationships.

We also saw a small uptick during the COVID-19 pandemic, when couples were forced into close quarters under stressful conditions.

So why are today’s high-cost times different?

It comes down to the type of stress.

A sudden crisis like COVID or a recession can push simmering tensions to breaking point. But today’s pressures, mortgages, rents, and day-to-day costs are long-term, structural challenges.

They don’t cause sudden fights; they quietly wear couples down.

Yet they also trap them, because leaving requires even more financial resources.

Later marriages, stronger unions, sometimes

Another factor in declining divorce rates is shifting demographics.

Australians are marrying later, often after years of cohabitation.

That means couples have already tested their relationship through multiple life stages before tying the knot.

Simon reflected on his own experience: “Sarah and I got married after we lived together for 14 years. By then, we’d lived through a gazillion crises. If it wasn’t working, we would have split earlier. So by the time we married, the foundations were solid.”

This trend means that fewer marriages happen, but those that do are generally stronger.

It also means people are more mature and self-aware when they marry, reducing the likelihood of impulsive choices that lead to regret.

Still, this doesn’t mean love is flourishing everywhere.

Many couples are together less because of affection and more because of economics.

The mental health trade-off

Staying together for financial reasons comes at a cost: well-being.

Census data consistently shows that the happiest people are those in stable, happy marriages.

Singles report lower average well-being, but the worst mental health outcomes come from those who are separated but not yet divorced.

Simon summarised it well:

“It is best to live in a happy marriage. But if your marriage isn’t working, it’s actually better for your mental health to break it up than to stay trapped.”

This suggests that while property prices may be lowering divorce rates, they may also be worsening mental health for those trapped in unhappy relationships.

Renting vs. owning: different pressures

The story looks a little different for renters.

Financially, separating is easier when you’re not tied to a mortgage; you simply end a lease and move out.

Renting also offers greater flexibility for those who anticipate lifestyle changes.

But here’s the catch: in tight rental markets, finding a new home isn’t easy.

A lack of supply can mean couples stay together longer than they’d like, simply because there’s nowhere else to go.

The gender shift in divorce economics

Historically, divorce tended to disadvantage women, who often had lower incomes and super balances.

Courts tried to compensate for this by adjusting asset splits in their favour.

But as Simon pointed out, this is changing:

“Women are outperforming men in education at every level, and in younger age brackets, they are already out-earning men. That means in 30 years, we may see the gender roles flip: men becoming the ones more disadvantaged in divorce.”

This reversal will reshape power dynamics within households and challenge long-held assumptions about financial vulnerability.

The bigger picture: housing as the silent influencer

This discussion is about more than relationships.

It highlights how deeply housing costs influence society.

High property prices don’t just delay homeownership.

They delay marriage, reshape family formation, influence fertility decisions, and even alter who has power in relationships.

Housing is quietly dictating who we love, how we live, and when we separate.

As Simon put it:

“Sooner or later, the housing angle pops up in almost every social issue. And usually, it’s in a disadvantageous way.”

Final thoughts

Choosing a life partner remains the most important decision we ever make; it shapes everything from our happiness to whether we have children.

But increasingly, that decision is being entangled with another: the housing market.

It’s a reminder that property is never just about bricks and mortar.

It’s about culture, relationships, and wellbeing.

As housing affordability continues to strain Australians, we’ll see more unintended consequences on the way we form and dissolve our most intimate bonds.

If you found this discussion helpful, don't forget to subscribe to our podcast and share it with others who might benefit.

]]>3Brett Warren<![CDATA[Every Cycle is Different: How Interest Rate Cuts Shape Australia’s Property Market]]>https://propertyupdate.com.au/?p=1910142025-08-26T01:10:06Z2025-08-27T07:30:53ZIf there’s one thing property investors learn over time, it’s that no two cycles are ever the same.

The past decade has reminded us of this lesson again and again.

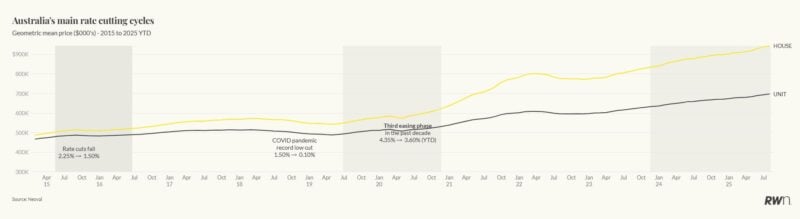

Since 2015, Australia has been through three major interest rate cutting cycles.

Each of these has played out very differently, with entirely different market segments benefiting depending on the broader economic backdrop and who was active in the market at the time.

And the way buyers respond to interest rate cuts is shaped just as much by affordability and demographics as it is by the cost of money itself.

Let’s take a look at a recent report by Nerida Conisbee explaining how these cycles unfolded—and more importantly, what lessons we can draw for the future.

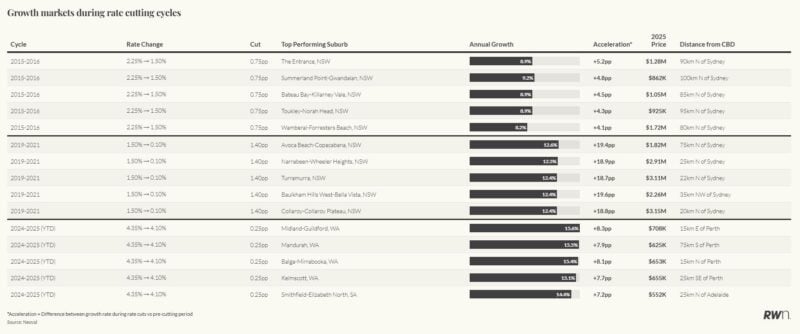

The First Cycle (2015–2016): coastal lifestyle markets rise

When the RBA eased rates from 2.25% down to 1.50% between May 2015 and May 2016, the biggest winners weren’t blue-chip suburbs but affordable coastal lifestyle locations close to Sydney.

The Central Coast was the standout, with Avoca Beach–Copacabana (8.0%), Wamberal–Forresters Beach (8.2%), and The Entrance (8.9%) all showing strong growth.

Conisbee explains:

“This was when the lifestyle shift really began.

People were seeking coastal living within commuting distance, and cheaper borrowing costs made that possible well before COVID accelerated the trend.”

These markets, priced between $800,000 and $1.2 million at the time, highlight how rate cuts can amplify emerging lifestyle preferences.

The Second Cycle (2019–2021): premium Sydney suburbs surge

The next phase was far more aggressive according to Conisbee.

From mid-2019 through the pandemic, rates plunged from 1.50% to just 0.10%.

This time, the response was concentrated in Sydney’s premium suburbs.

Castle Hill, Baulkham Hills West–Bella Vista, and Northern Beaches areas like Collaroy and Freshwater all recorded double-digit growth.

Baulkham Hills West–Bella Vista alone swung from -7.2% to +12.4% growth, a 19.6 percentage point acceleration.

According to Conisbee:

“Ultra-low rates and fiscal stimulus created a pronounced wealth effect.

Established property owners, particularly in Sydney’s premium markets, were able to upgrade or expand their portfolios.

It wasn’t first home buyers driving this cycle, it was the affluent.”

This was a clear reminder that rate cuts don’t always make property more accessible, they can just as easily amplify demand where wealth is already concentrated.

The Third Cycle (2024–2025): affordable outer suburbs take the lead

Fast forward to today, and we’re in another cutting cycle; this time from the highest interest rates seen in over a decade.

But instead of boosting premium markets, affordability has become the driving factor.

Perth’s Midland–Guildford (15.6%), Mandurah (15.5%), and Balga–Mirrabooka (15.4%) are leading national growth.

In Adelaide, Smithfield–Elizabeth North is up 14.4%.

These are outer suburban markets priced between $550,000 and $750,000—very much first home buyer territory.

Conisbee notes:

“Unlike the COVID cycle, today’s cuts are most effective for buyers on the margins of borrowing capacity.

Affordable outer suburbs are where interest rate reductions translate directly into stronger demand.”

In other words, the affordability crisis has fundamentally reshaped who benefits when monetary policy loosens.

The consistent performers

While the beneficiaries have shifted from lifestyle seekers, to wealthy upgraders, to first home buyers, some regions have shown enduring sensitivity to rate cuts.

Conisbee highlights:

“The Central Coast is fascinating. Across all three cycles, it’s shown consistent growth.

That tells us some markets retain a structural advantage, whether that’s lifestyle appeal, location, or ongoing affordability relative to Sydney.”

Key lessons for investors

What should investors take away from this decade-long story?

Each cycle has its own winners. As Conisbee says, “We can’t assume that because one group benefited in the past, they’ll benefit again.”

Affordability now matters more than ever. Today’s rate-sensitive suburbs are not the million-dollar enclaves, they’re the $550k to $750k markets.

Some markets have lasting resilience. Places like the Central Coast show that structural appeal can cut across multiple cycles.

Context is everything. Fiscal stimulus, global shocks like COVID, and demographic shifts shape how rate cuts flow through the market.

Final thoughts - a new window of opportunity

The past decade of rate cycles proves just how dynamic and unpredictable Australia’s property market really is.

Conisbee sums it up well:

“Every cycle is different.

The beneficiaries shift depending on affordability, economic conditions, and who’s active in the market.

Understanding that context is critical for investors.”

As we look ahead, it’s clear that today’s easing is delivering the greatest benefits to outer suburban, affordable markets.

That’s a profound shift from the wealth-driven gains of the COVID cycle, and a reminder that strategy, not just timing, is what separates smart investors from the rest.

However, one thing is clear: there's currently a window of opportunity for property investors with a long-term focus.

Right now, we’re seeing what some would call a “perfect storm” of fundamentals that are aligning to support strong property markets in the years ahead:

Continued rapid population growth is putting pressure on housing.

An acute undersupply of dwellings,

A chronic shortage of skilled labour, making new development slower and more expensive.

Inflation has moderated, now sitting within the RBA’s target range.

Interest rates will keep falling – bringing more buyers into the market

Government first homebuyer incentives will pour fuel on the flames of our undersupplied housing market.

As interest rates keep falling and confidence returns among both buyers and sellers, we’ll enter the next phase of the property cycle.

And historically, this stage has delivered some of the best capital growth for those who act early.

Are you clear on how to take advantage of these market conditions — or are you still waiting for "certainty"?

]]>0Ken Raisshttps://wealthadvisory.metropole.com.au/<![CDATA[Are you as good with money as you think you are?]]>https://propertyupdate.com.au/?p=951742025-08-26T01:09:51Z2025-08-27T04:00:36ZA lot of people say they’re good with money.

They say they have a gift for making it.

That they love money and that money loves them.

This may be true.

But just because you like money and enjoy making it (that’s most of us) doesn’t mean you’re good with money.

Those are two very different things.

What does it take to be good with money?

Restraint for one.

Self-knowledge is important, too.

Understanding how money works also goes hand in hand with being an expert at it.

So do you want to know if you’re really good with money?

Well, see how many of the following boxes you tick:

1. You don’t listen to barbecue advice

If I had a dollar every time someone recommended that I check this new business idea or investment scheme when I was at a barbecue, I would be a very rich man indeed.

If you’re good with money — truly good with money — then you’re not easily swayed by the advice of people, who may be very nice and well-meaning but are not experts at investments.

People who know money only listen to experts.

The barbecue, after all, is for footy and fishing talk.

2. You know the difference between good debt and bad debt

Some people think they’re good with money because they look expensive.

They wear the right clothes and drive expensive cars.

But getting a loan or a credit card to do these things doesn’t make you rich.

It makes you foolish.

Bad debt is a credit card debt or a loan against a depreciating asset.

Better to owe $150,000 on a house (presuming you have the means to pay it off) that is appreciating than to have a $5,000 credit card debt with an 18 per cent interest rate.

3. You know how much super you have

And not only that, you know how your super fund performs each year.

You know the name of the fund, where that money is invested, and how other super funds are performing.

If you have a self-managed super fund you take an even more active role in tracking the performance of your investments.

You know how much you pay in fees and how various stocks are performing.

You may not work in finance, but you take an active interest in your retirement and money because you understand how important it is.

4. You know your credit score

There are no excuses these days for not knowing your credit score.

It’s very easy, too, to find out what yours is.

Anytime you apply for credit, the lender will look at your score to decide your credit rating.

This final point is the real clincher because being good with money is about not worrying about being good with money.

The ultimate sign that you are good with finances is the fact you don’t stress about them.

You don’t stress because you don’t need to.

You know exactly what you’re doing and you understand your finances fully.

Hopefully, I’ve given you some food for thought.

The truth is all of us could be better with money.

No matter how accomplished we become, we always have room for improvement.

There's no time like the present to start is there?

Disclaimer

This article is general information only and is intended as educational material. Metropole Wealth Advisory nor its associated or related entitles, directors, officers or employees intend this material to be advice either actual or implied. You should not act on any of the above without first seeking specific advice taking into account your circumstances and objectives.

]]>0Michael Yardneyhttps://michaelyardney.com<![CDATA[8 Essential Books You Should Have in Your Library]]>https://propertyupdate.com.au/?p=1478172025-07-31T02:39:51Z2025-08-27T00:30:00ZIt has been said that the most important factors that will change where you are in 12 months’ time compared to where you are today in your life are the books you read and the people you hang around with.

If you want to improve your life, I believe you need to build the foundations of success by honing three sets of fundamental skills.

Mindset skills

People Skills

System skills – the techniques you require for whatever investment system you choose, such as Real Estate or share market skills, or the internet skills you need.

So, let’s look at some of the books you should read over the next few months to help you improve those 3 sets of skills.

These are the foundational books that you need to read or reread to help set yourself up for the future.

Mindset Skills Books

1. Think and Grow Rich by Napoleon Hill

This book is on the bookshelf with every successful investor and entrepreneur

While this is a very old book now, and a little bit difficult to read, you will find most successful people will say this was one of the foundational books that got them going having sold over 100 million copies.

Sure, this is one of my books, but it has become an international bestseller and translated into 5 foreign languages.

Rich people think a certain way and poor people think a completely different way, and those ways of thinking determine their actions and therefore determine their results.

Just study the Rich and copy their Rich Habits is the advice of my co-author Tom Corley and me.

We explain that we are where we are because of the things we do day in, and day out.

Our old ways of thinking, and our old habits brought us exactly to where we are and if we want something to be different in our lives, we need to do something different.

This book debunks the myths and “common wisdom” about how to get rich.

Read it to unlock the secrets to success and failure, based on Tom Corley’s five years’ study of the daily activities of 233 rich people and 128 poor people as the authors expose the immense difference between the habits of the rich and the poor.

Since the release of Rich Habits Poor Habits in 2016, I’m proud to say that Tom Corley and I have gone on to share the mindset secrets of the rich and successful to new and bigger audiences and this book has become an international bestseller and is being translated into 5 foreign languages.

It will help you understand how the rich think very, very differently from the poor.

Tom Corley and I explain how the way your life looks today is a result of the choices you have made which are the results of the often unconscious habits you’ve developed.

People Skills Books

3. How to Win Friends and Influence People - Dale Carnegie

You probably have heard of this book, have you read it?

It’s one of the classic books on people skills.

4. The Seven Habits of Highly Effective People – Steven R Covey

This is another classic, and an example of why you don’t need to read brand-new books.

How many of the habits of highly effective people have you incorporated into your life?

5. Influence – by Robert Cialdini

I still remember buying the tape set of this back in the early 1990s.

This was long before they were audiobooks.

I listen to the audio and it changed my life, how I deal with people and how I negotiate influence and persuade.

Dr Cialdini taught me the six fundamentals of influence which are part of my DNA today and which I just got in more detail in my book – Negotiate Influence Persuade.

6. Negotiate, Influence, Persuade

This is another one of my books which has been translated into 5 languages and is an international best seller, where I teach you how to get other people to want to do what you want them to do because of your ability to interact, communicate, negotiate, influence and persuade.

In every transaction there is a buyer and a seller: they either buy what you’re saying, or you buy what they’re saying.

But this book is not just for salespeople, it’s also for you as a consumer because we all negotiate every day of our lives. Not just in business but in day-to-day life with your spouse, your children, your work colleagues, your customers or your clients.

While plenty of books teach sales and negotiation techniques, this one explains the fundamentals and the psychology behind why these techniques work and how to use them most effectively. It’s more than just a book about negotiation. It’s about persuasion and influence, and more importantly, how to wield those two important traits to meet your goals.

It will change how readers will do business, and how they will interact with their family and friends and hopefully give them a greater understanding of why people behave and are motivated to act, the way they do.

Click here now and buy your copy. Imagine how different your life will be when you develop your skills, realise your full potential and make your life work.

System Skills Books

7. Rich Dad Poor Dad: What the Rich Teach Their Kids About Money – That the Poor and Middle Class Do Not! by Robert T. Kiyosaki

While this book was more than 20 years ago, its insights stand the test of time.

Kiyosaki also offers personal finance advice and breaks down money misconceptions across a broad spectrum.

Robert’s story of growing up with two dads — his real father and the father of his best friend, his rich dad — and the ways in which both men shaped his thoughts about money and investing.

The book explodes the myth that you need to earn a high income to be rich and explains the difference between working for money and having your money work for you.

However, be careful – some of Kiyosaki’s property strategies don’t translate well to Australia where the rules are different to the USA, because in Australia investing for capital growth is the way to go.

This new totally updated, 20th-anniversary edition of the best seller is a must for all property investors as it outlines a framework to build financial freedom in the new economic climate.

This book has become the property investment classic and is on the bookshelf of almost every successful Australian property investor.

Readers receive a time-proven step-by-step action plan showing how to achieve real wealth through property investment and learn how to live the life of a property multi-millionaire using my pyramiding system to buy more properties with no money out of your own pocket.

This book is suitable for beginners, yet has advanced strategies for experienced investors.

There you have it, a list of books that you should read and reread to build up your skill set.

And yes, I am touting some of my books, but having said that I know the success so many readers have achieved from the lessons they have learned in these books, so I’d be wrong if I didn’t give you the opportunity of getting the same great results by changing your skill sets.

I believe you should read these books, or re-read them before you read any of the new books.

If you haven’t incorporated the fundamental principles you’ll learn from these books into your life, what can you book teach you?

You need strong foundations to build your multi-million dollar property portfolio.

If you don’t have strong foundations the whole thing could topple over.

]]>4Michael Yardneyhttps://michaelyardney.com<![CDATA[Latest Property Price Forecasts Revealed. Australian Property Market Outlook 2025–26: Where Prices Are Headed After Three Rate Cuts.]]>https://propertyupdate.com.au/?p=1142892025-08-27T07:17:21Z2025-08-26T22:00:39Z

Australia’s property markets are on the move again.

After a period of fragmented property price growth and cautious sentiment, recent developments have brought momentum back into the picture.

The Reserve Bank of Australia has delivered three interest rate cuts this year — most recently lowering the official cash rate to around 3.6% — easing borrowing costs and sparking renewed appetite among buyers.

Home values are climbing steadily, auctions are heating up, and investor activity is surging.

Yet balance remains: affordability remains stretched, supply shortages persist, and not all buyers benefit equally.

However, I see this as the beginning of a new property supercycle. Not a boom, but a period of prolonged property price growth.

But as always, the markets will remain fragmented.

This latest upswing doesn’t negate the fundamentals we laid out previously — Australia’s property market remains underpinned by resilient households, tight supply, and divergent cycles across cities.

What has changed is the tone of the cycle. Where we once saw caution and fragmented performance, we’re now witnessing across-the-board value growth and renewed buyer confidence.

That doesn’t mean the story’s shifted completely — elements like lending buffers, affordability constraints, and ongoing supply shortfalls continue to shape how different markets perform.

In the sections that follow, I am going to revisit revisit my forecasts with fresh eyes — layering in the impact of rate cuts, auction activity, and shifting investor sentiment to help you navigate what really matters for the next 12–24 months.

Every capital city recorded a rise in dwelling values through the month - led by Darwin with a solid 2.2% rise, followed by Perth, up 0.9%. At the softer end of the growth tables are Hobart (+0.1%), Melbourne (+0.4%) and the ACT (+0.5%).

The latest PropTrack Home Price Index similarly reported that national home prices hit a new record high of $827,000 in July, following a rise of 0.3% over the month and 4.9% over the year.

In early April US President Donald Trump announced range of tariffs which posed a significant downside risk to global trade and economic growth but then swiftly reversed them.

Of course global trade tensions pose a significant risk to the world's economic outlook and Australia is not immune, but like all things with Donald Trump, the situation remains fluid and the final outcome remains uncertain.

One of the most significant impacts of Trump's tariffs has been on interest rate forecasts.

The uncertainty and potential slowdown in economic activity has led to increased speculation that central banks, including the Reserve Bank of Australia (RBA), might lower interest rates even more than previously expected to bolster the economy.

NAB executive chief economist Sally Auld now expects easing interest rates to support property growth and the economy to have a “soft landing” with inflation settling around the middle of the RBA’s target band by the second half of this year and unemployment staying below 4.5pc.

“That said, there are building headwinds in the global economy and shifts in US trade policy are likely to be net disinflationary for Australia.

Consequently, the RBA will need to normalise rates quickly to ensure policy is appropriately calibrated. We now see the RBA cutting to 3.1pc by August and then taking the cash rate to 2.6pc by early-2026.”

The cash rate target was last at 2.6pc in October 2022 – which was at the tail end of pandemic lockdowns.

Of course lower interest rates make borrowing more affordable and in general stimulate our property markets.

There is still a window of opportunity for property buyers to get into the market before further falls in interest rates cause a new flurry of activity later in the year.

The share market’s drama after Trump’s tariff announcements (and re-announcements) reminded me why I invest in property.

There’s something strangely comforting about the opacity of property prices during market turmoil. You can’t obsessively check your property value twenty times a day (though I know a few who’d try if they could).

This information gap might seem frustrating at times, but it’s actually a psychological superpower. It prevents panic selling. It forces long-term thinking.

And it stops you making decisions in the heat of emotion that you’ll regret when cooler heads prevail.

Note: Don't make 30 year investment decisions based on the last 30 minutes of news.

Sure there are turbulent times ahead, but our housing markets are well positioned to weather them.

RBA data shows that less than 1% of households are in negative equity, a vast improvement from around 1.5% in early 2019 before Covid.

The majority of mortgage holders have loan-to-valuation ratios well below 80%, with many clustered in the 40–60% range.

In fact 50% of home owners have paid off their mortgage.

This means that, even if Australia has an economic downturn and unemployment rises, most borrowers have the flexibility to manage their situation — including the ability to sell without taking a loss.

Sure recent borrowers with high debt levels and thinner buffers are more at risk, but forced sales are likely to remain low, even if unemployment rises.

This overall financial resilience of Australian households is a critical cushion for both the property market and broader economic stability.

Back to what's happening in the Australian Property Markets

Of course, each state is at its own stage of the property cycle and within each capital city there are multiple markets.

While regional property markets became popular with homebuyers wishing to escape Covid a couple of years ago, and more recently regional markets were attractive to investors because of their comparatively lower prices, over the long term capital city property markets have outpaced regional areas and this trend is likely to continue.

Overall, persistently low supply relative to demand are supporting housing values despite high interest rates, ongoing cost of living pressures, worsening affordability pressures and a deeply pessimistic level of consumer confidence.

The gap between capital city house and unit values has widened substantially.

Capital city house values rose almost 3 times as much as unit values since the onset of Covid... but the gap is narrowing across most cities.

And after underperforming throughout the pandemic period, unit prices recorded stronger growth for much of 2025 as affordability constraints will mean more Australians trade backyards for balconies and courtyards this year.

However the chart below shows the significant gap in property price growth between these two types of dwellings.

The good news is that this creates a window of opportunity, as one can now buy established family friendly apartments considerably below replacement cost.

Here's the forecast for property prices in 2025-26

Domain’s latest Price Forecast Report for FY25-26 reveals that Australia’s property market is expected to see continued price growth over the next 12 months, with major capital cities Sydney and Melbourne driving national trends.

Unlike the turbocharged growth of the post-COVID boom or the sharp rebounds of past rate-cutting cycles, this future upswing will be defined by subtle shifts in momentum, affordability limits, and policy intervention.

The range of capital city price growth is expected to narrow.

Sydney and Melbourne are forecast to lead, as they typically respond more quickly to interest rate changes. Meanwhile, Adelaide and Perth – standout performers over recent years – are expected to experience slower positive growth as affordability constraints intensify.

Brisbane unit prices are expected to moderate from the previously unsustainable double-digit growth, while house prices continue to grow at a pace similar to that of last year.

Domain's House price forecasts

HOUSES | STRATIFIED MEDIAN PRICE

ANNUAL CHANGE

LEVEL

RECORD

BELOW PEAK

Capital City

FY25

FY26

FY25

FY26

FY26

FY26

Sydney

4%

7%

$1,717,107

$1,829,576

YES

Melbourne

0%

6%

$1,046,246

$1,112,623

YES

Brisbane

5%

5%

$1,037,357

$1,093,414

YES

Adelaide

12%

4%

$1,013,204

$1,049,117

YES

Canberra

-2%

4%

$934,225

$981,808

NO

-7%

Perth

7%

5%

$934,225

$981,808

YES

Combined capitals

4%

6%

$1,194,942

$1,264,614

YES

Domain's Unit price forecasts

UNITS | STRATIFIED MEDIAN PRICE

ANNUAL CHANGE

LEVEL

RECORD

BELOW PEAK

Capital City

FY25

FY26

FY25

FY26

FY26

FY26

Sydney

3%

6%

$835,819

$888,822

YES

Melbourne

-3%

5%

$555,522

$584,400

NO

-3%

Brisbane

12%

5%

$670,798

$701,490

YES

Adelaide

10%

3%

$568,000

$586,366

YES

Canberra

-13%

3%

$531,784

$546,265

NO

-15%

Perth

12%

6%

$519,551

$552,487

YES

Combined capitals

3%

5%

$680,568

$717,266

YES

History suggests that once rates start falling, property prices don’t wait around.

Bank of Queensland chief economist Peter Munckton has crunched four decades of data which was reported in the Financial Review and said a 10 to 15 per cent price rise over the next two years is a reasonable bet – no matter how many cuts the RBA ends up delivering.

Munckton explained...

“There were smaller price rises in both the early 1980s and 1990s.

But on both those occasions, the unemployment rate was above 10 per cent.

Currently, the unemployment rate is within touching distance of 50-year lows,”

On the flip side, Munckton says the extraordinary 20 per cent-plus gains seen in the ’80s, ’00s and during the pandemic also seem off the cards over the next couple of years

Tip: The expansion of the first homebuyer support will add further fuel to our housing markets

From January 1 2026, virtually all first home buyers will be able to enter the market with just a 5 per cent deposit, via a taxpayer-backed guarantee.

This part of his election promise, prime minister Anthony Albanese promised to turbocharge the program by scrapping the $125,000 income cap, making it available to an unlimited number of applicants instead of just 35,000 per year, and dramatically raising property price thresholds.

A separate promise to build 100,000 new homes was also made – but that extra supply could take years to arrive, if it arrives at all.

You can always beat the averages.

While it’s likely that property price growth will take off in the second half of 2025, the good news is that you can always beat it by investing in the right property in the right location.

Now by that, I don’t mean look for the next hotspot.

I mean buying quality properties in locations that will outperform in the long term such as gentrifying suburbs.

You see...property offers countless opportunities to improve your results through your own time, skills and knowledge – so you don’t need to settle for average.

And there’s more to it than just location. You can add value through refurbishment, or redevelopment.

What does the third RBA interest rate cut mean for our housing markets?

Knowing the Board’s strong preference for quarterly inflation data, it will likely wait until the 3-4 November meeting before cutting the cash rate again, provided the September quarterly CPI results, due out on 29 October, remain on track.

Current big four bank cash rate forecasts

Bank

Next cut

Total no. cuts to come

Cash rate at end of cuts

CBA

4 November

1

3.35%

Westpac

4 November

3

2.85%

NAB

4 November

2

3.10%

ANZ

4 November

1

3.35%

A single 0.25 percentage point cash rate cut, if fully passed on by lenders, could reduce monthly repayments on a $600,000, 25-year mortgage by $90.

If Westpac’s forecast plays out, with four rate cuts through to mid-next year, homeowners could see a total drop of $349 a month.

Impact of four potential rate cuts

Monthly repayments

Total change from today

Current

$3,793

-

1 cut

$3,703

-$90

2 cuts

$3,615

-$178

3 cuts

$3,528

-$265

4 cuts

$3,444

-$349

Source: www.canstar.com.au. Notes: based on owner-occupier paying principal and interest with 25 years remaining in July 2025 on the estimated RBA average variable rate of 5.80%. Assumes cash rates cut are in August, November, February and May and passed on in full the month after.

However, the benefits from the rate cut will not be distributed equally.

High-income earners with significant equity in their properties are likely to feel more confident in re-entering the property market than Aussie battlers who have been hurt by the cost of living crisis and who are unlikely to notice a significant change in their budget with this 0.25% cut in their mortgage rates.

Historically, when interest rates fall, buyers who have been sitting on the sidelines are enticed back into the market and property values start to increase as buyer confidence increases before seller confidence, making these new home buyers compete for the limited stock of properties available.

Traditionally, the premium suburbs in Sydney and Melbourne have led the market in price rebounds after interest rate cuts.

This time around it is likely that the 0.25% interest rate cut will stabilise house prices in Melbourne and Sydney, which have been falling over the last few months, rather than igniting the next phase of the property cycle.

The increased confidence brought about by the drop in interest rates may be all the Melbourne housing market needed to pick up from its four-year slump.

While the affordable end of the Melbourne market out performed over the last few years, as more affluent homeowners “sat on their hands”, it is like the increased confidence that the interest rate drop will bring will now encourage these homeowners to get on with their life plans.

And with Melbourne being relatively cheap compared to other cities, more and more property investors are taking advantage of the window of opportunity to get into Australia’s second biggest housing markets prices that won’t be available in a year or two's time.

How can values continue rising amid high interest rates and the cost of living crisis?

Clearly affordability has decreased, but the housing markets are being underpinned by a number of factors:

Wealthy buyers entering the market with higher deposits.

Downsizers who had a lot of equity in their homes are buying debt free - in fact a third of properties last year were transacted with no mortgage at all.

The bank of mum and dad and inheritances are helping many buyers with a deposit.

The recent first home buyer incentives offered by both major political parties will increase demand at a time of lack of supply further pushing up prices, especially at the lower end of the market.

Some buyers are buying in cheaper markets while others are buying units rather than houses.

Rentvestors will keep buying investment properties while renting in their preferred living locations

The latest housing market stats

Corelogic report similar figures to Proptrack suggesting that in annual terms, Australian home values were up 4.9% in 2024, adding approximately $38,000 to the median value of a home.

Here are the latest stats provided by CoreLogic for property price changes around Australia:

Index results as at 31st July 2025

Change in dwelling values

Month

Quarter

Annual

Total return

Median value

Sydney

0.6%

1.8%

1.6%

4.6

$1,228,435

Melbourne

0.4%

1.2%

0.5%

4.3%

$803,424

Brisbane

0.7%

2.3%

7.3%

11.1%

$934,623

Adelaide

0.7%

1.5%

7.0%

10.8%

$843,339

Perth

0.9%

2.6%

6.5%

11.0%

$831,921

Hobart

0.1%

0.1%

1.9%

6.3%

$673,383

Darwin

2.2%

5.6%

8.5%

15.8%

$549,371

Canberra

0.5%

1.3%

0.5%

4.5%

$861,281

Combined capitals

0.6%

1.8%

3.0%

6.5%

$926,854

Combined regional

0.6%

1.7%

5.9%

10.5%

$689,369

National

0.6%

1.8%

3.7%

7.4%

$844,197

Source: Cotality HVI 1st August 2025.

We also keep track of “Asking Prices” as these are a good leading indicator for the property market because they reflect the sentiment of sellers and their expectations for the future value of their homes.

Sydney Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

2,051,858

15.042

0.6%

7.0%

All Units

867,183

-6.983

-1.2%

4.3%

Combined

1,565,182

6.070

0.2%

6.1%

Source:SQM Research, August 2025

Melbourne Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,289,507

-1.707

-0.4%

4.3%

All Units

636,530

0.860

1.1%

4.4%

Combined

1,083,092

-0.896

-0.2%

4.2%

Source:SQM Research, August 2025

Brisbane Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,273,880

5.680

1.2%

10.2%

All Units

751,263

4.987

1.8%

16.7%

Combined

1,142,398

5.506

1.3%

11.1%

Source:SQM Research, August 2025

Perth Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,165,722

10.612

1.8%

10.4%

All Units

663,673

3.176

1.2%

19.5%

Combined

1,034,145

8.663

1.7%

11.8%

Source:SQM Research, August 2025

Adelaide Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,053,445

3.785

0.7%

12.5%

All Units

569,360

6.030

1.0%

22.8%

Combined

966,342

4.189

0.7%

13.5%

Source:SQM Research, August 2025

Canberra Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,236,492

5.008

1.6%

4.5%

All Units

589,142

0.583

-0.7%

0.5%

Combined

994,347

3.353

1.1%

3.1%

Source:SQM Research, August 2025

Darwin Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

790,078

-3.078

-1.5%

22.0%

All Units

443,636

3.739

5.0%

16.0%

Combined

653,899

-0.398

0.2%

20.3%

Source:SQM Research, August 2025

Hobart Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

845,845

4.791

0.1%

7.5%

All Units

499,047

0.353

0.5%

2.7%

Combined

792,981

4.115

0.2%

6.9%

Source:SQM Research, August 2025

National Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,012,356

3.997

1.5%

8.4%

All Units

597,340

2.386

1.1%

7.1%

Combined

922,500

3.648

1.4%

8.1%

Source:SQM Research, August 2025

Capital Cities Property Asking Prices

Property type

Price ($)

Weekly Change

Monthly Change %

Annual % change

All Houses

1,493,248

13.842

1.6%

7.5%

All Units

740,975

-0.801

-0.7%

6.9%

Combined

1,268,953

9.476

1.2%

7.2%

Source:SQM Research, August 2025

The fundamentals of what drives Australian property prices

If you take a telescopic view, rather than a microscopic view, and look at what's ahead for housing markets over the next decade or two, the two big factors driving our housing markets will be demographics (how many of us there are, have we want to live and where we want to live) and the wealth of the nation.

But first, let’s dig a bit deeper into the key underlying factors that will be influencing our property markets in the medium term.

1. Interest rates/affordability

While many people believe interest rates are a key driver of property values, and that's why there were so many pessimistic property forecasts as interest rates rose through 2022-23, our housing markets showed considerable resilience and kept rising in value despite the 13 interest rate rises the RBA threw at us.

Of course, falling interest rates and the subsequent increased affordability are strong drivers of property price growth, but the reverse isn't true.

House prices are driven by many other factors, not just interest rates, but rates are on the way down.

2. Supply and demand

Housing supply has a significant influence over house prices in the short term: an undersupply puts pressure on prices to rise while an oversupply does the opposite.

Despite very strong population growth, we’re just not building enough new dwellings, and this has put pressure on housing supply reflected in low rental vacancy rates and higher house prices.

At the same time, the strong absorption of new listings for sale has kept total listings in the market suppressed, intensifying competition between buyers.

These factors have created a sharp shortage of housing, outweighing the negative impact of rates on prices.

And there is no end in sight as building approvals (which are a good indication of future supply) are running at very low levels.

And just because a new apartment complex has been approved, it doesn't mean it will get built.

At the moment very few new complexes are coming out of the ground because it's not financially viable to build them at today's market prices.

Of course, this means future new developments will have to sell at prices considerably higher than today’s market value and this will, in turn, pull up the value of established apartments.

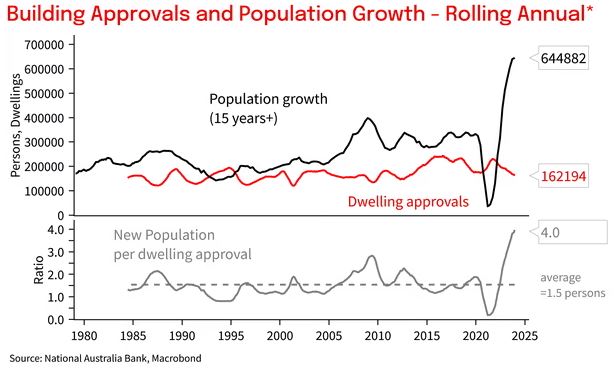

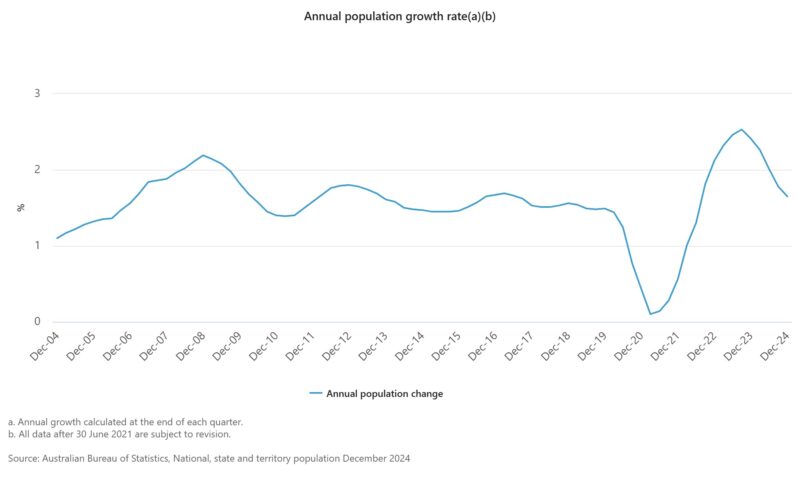

The surge in population growth to a record 660,000 last year, driven by record immigration levels meant that around an extra 250,000 new homes needed to be built last year alone.

But instead, completions have been running around 170,000 as the home building industry struggles to keep up with rising costs and material and labour shortages and as approvals to build new homes fell.

In fact it has been "conservatively" estimated that we have an accumulated housing shortage of around 200,000 dwelling currently, and it is unlikely our housing shortage will be resolved in the next decade, maybe we will have continue continuing pressure for rising house prices and rents.

3. Consumer confidence

Consumer confidence is a critical factor affecting the direction of property prices.

We don't make big financial decisions like moving home or buying an investment property unless we feel confident about our economic future and our financial stability.

Consumer confidence has been at historic lows because of all the economic and socio-political issues that have confronted us, but has picked up recently.

I believe that during 2025 consumer confidence will continue to rise as it becomes obvious that inflation is under control and interest rates will eventually fall.

At the same time, the “wealth effect” of an improving economy and rising property values will lead to further consumer confidence and bring home buyers and sellers back into the market.

4. Economic climate

Another key factor that affects the value of the property market is the overall health of the economy.

This is generally measured by economic indicators such as the gross domestic product (GDP), employment data, manufacturing activity, the prices of goods, etc.

While the RBA has been trying to slow our economy down to bring inflation under control, currently, everybody who wants a job can get a job and this will underpin our housing markets even if the economy falters a little moving forward.

5. Population growth

In the year ending 30 June 2024, overseas migration contributed a net gain of 446,000 people to Australia's population.

This was a decrease from the record 536,000 people the previous year once the floodgates were opened as we worked our way out of the Covid Pandemic.

While population growth has always been a key driver supporting our property markets, the influx over the last few yearshas pushed our supply/demand balance off-kilter and is key to the increase in housing prices and the shortage of rental properties.

6. Availability of credit

When the credit (the ability to borrow from the banks) is readily accessible, with lower interest rates and less stringent lending criteria, it tends to stimulate the housing market since more people find themselves able to borrow money to buy homes, leading to increased demand for housing.

On the flip side, when credit is tightened through higher interest rates or stricter lending criteria (as happened when APRA made the banks tighten the purse strings in 2016-7), the effect can be a cooling of the housing market.

Such measures are usually a deliberate policy response to an overheated market, aiming to reduce the risk of a “property bubble” and subsequent crash.

7. Investor Sentiment

This sentiment, essentially the collective attitude and outlook of investors towards property markets, can significantly influence both the demand for and the value of real estate.

Investors generally account for around one-third of all property transactions so positive investor sentiment can drive up property prices, especially in sought-after areas.

Conversely, negative investor sentiment, as occurred during the market downturn of 2022, can lead to a decrease in property values.

If investors believe that property prices will stagnate or fall, they may be less inclined to invest, or they might choose to sell off their properties, increasing supply in the market.

8. Government incentives

Government incentives can have both direct and indirect impacts on the real estate sector.

One of the most direct ways government incentives affect property values is through policies aimed at stimulating demand.

For instance, initiatives like the First Home Owner Grant (FHOG) or stamp duty concessions for first-time buyers directly increase buying capacity, leading to greater demand for property.

Another aspect is the development incentives provided by the government to promote specific types of property development, such as high-density housing or urban renewal projects.

These incentives can increase property values in targeted areas by improving infrastructure, accessibility, and community facilities, making them more desirable places to live.

Tax policies and regulations also play a crucial role.

Negative gearing can increase demand for investment properties, pushing up prices.

And every time there is talk about removing negative gearing or amending taxes including land tax, investors shy away from our housing markets.

Australian housing market predictions for 2025 and 2026

The last few years have shown us how hard it is to forecast property trends, and as always there will be headwinds and tailwinds buffeting our property markets.

Currently Australia’s housing is so undersupplied that I've rarely encountered a supply-demand inflection point like this that requires such attention.

And it’s only going to get worse.

Drivers of property price growth in 2025 will include:

Continued strong population growth at a time when we are not producing enough supply of new dwellings. This extreme shortfall will exert upward pressure on house prices and rents throughout 2025.

Interest rates will continue to fall through 2025 and at some stage it is likely APRA will relax its mortgage serviceability buffer. This is currently at 3% and the combination of these factors will increase borrowing capacity.

FOMO (fear of missing out) will creep in as buyers realise that real estate values are rising and as the media will keep mentioning new record prices being achieved.

Headwinds:

Stretched affordability will remain an issue in 2025, however, buyers will want to get on with their lives and therefore choose townhouses or apartments over homes or move to more affordable suburbs.

Geopolitical problems and talk about a recession may lead to some financial uncertainty and worries about job security which could stop some buyers from making important decisions like buying a home or an investment property.

Poor consumer sentiment was a feature of much of the last few years, holding back property buying decisions, and until there is more certainty about our economy and confidence that interest rates have peaked and inflation is under control, it's likely that consumer confidence will remain low until interest rates start falling.

The strongest performers are likely to be Brisbane and Perth, where population growth is expected to outpace supply more than in other cities.

With the increase in value of houses strongly outpacing the apartment market recently, now with the differential in price between units and houses at the highest level on record, and with houses becoming more unaffordable for many, I can see strong capital growth ahead for family-friendly apartments in great neighbourhoods.

8 economic and property trends to watch out for moving forward

1. The recovery phase of the market will continue throughout 2025

Property price growth will continue throughout 2025, albeit at a much lower rate and our housing markets will be fragmented as affordability will affect many homebuyers.

2. Interest rates will fall

Interest rates will keep falling over the year with probably a rate cute every 3 months (quarterly) and this will likely encourage greater housing investment and more homebuyers.

3. Our property market will be even more fragmented

Of course, there was really never "one" Sydney property market or one Melbourne property market.

There are markets within markets – there are houses, apartments, townhouses and villa units located in the outer suburbs, middle ring suburbs, inner suburbs and the CBD, and they're all behaving differently.

But our markets will be much more fragmented moving forward as some demographics struggle with cost-of-living, rent and mortgage cost increases (at a time of low wage growth) more than others.

It will either stop them from getting into the property markets or severely restrict their borrowing capacity which will negatively impact the lower end of the property markets.

Meanwhile, many first-home buyers who borrowed to their full capacity will have difficulty keeping up with their mortgage payments at the time of rising interest rates or when their fixed-rate loans convert to variable rates.

In other words, there will be little impetus for capital growth at the lower end of the property market.